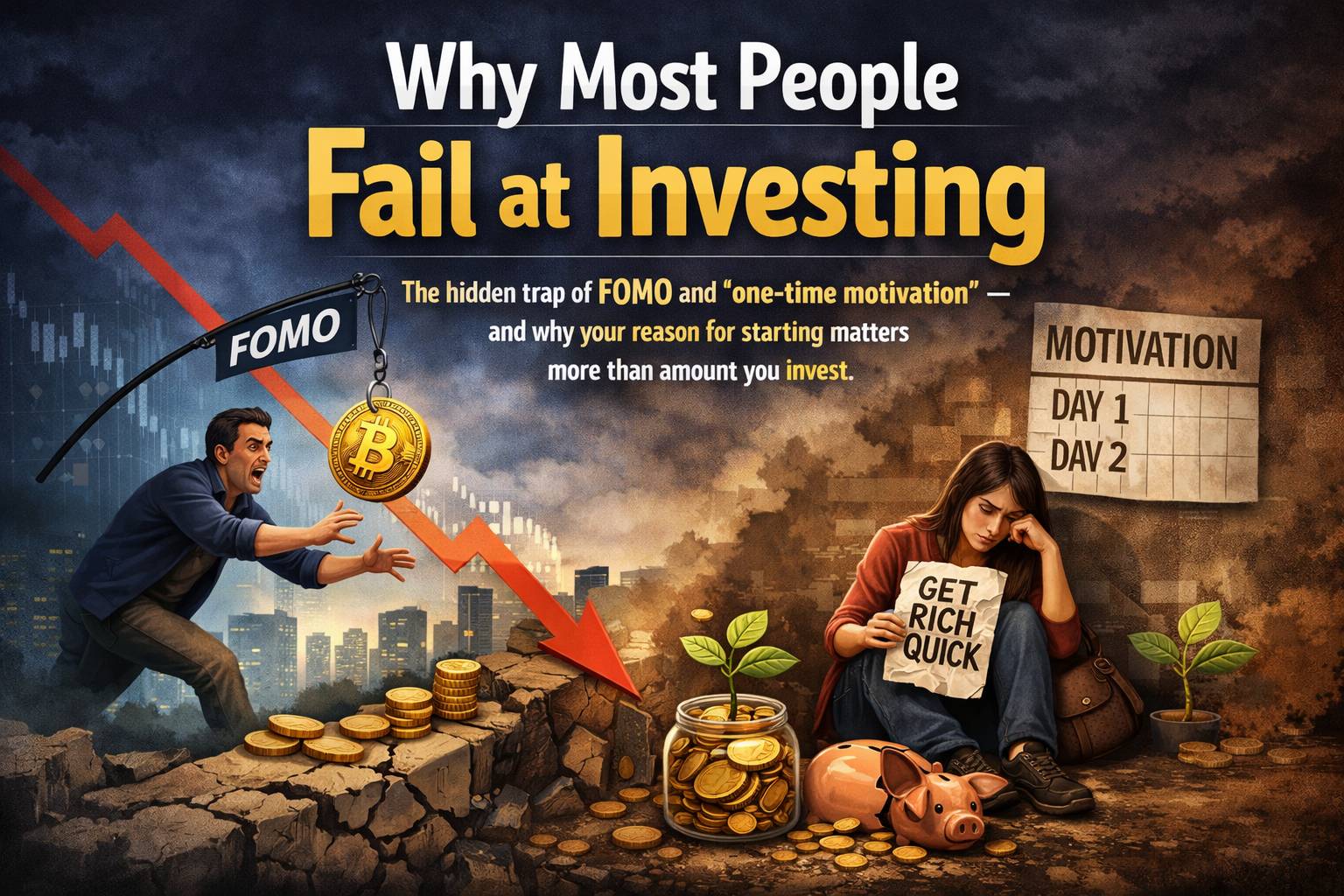

Every January, thousands of people receive mutual fund gift cards at weddings, Diwali celebrations, or corporate events. Every time the market rallies 40% in a calendar year, a fresh wave of investors floods in — inspired by a colleague's boast over lunch or a cousin's dinner-table story. Both groups begin with genuine excitement. And most of them quietly disappear within 12 to 18 months.

This is not a story about market returns. This is a story about why people invest in the first place — and why that reason determines everything that follows.

The Core InsightMost investors fail not because markets are unkind — but because they started for the wrong reasons. External triggers create temporary action. Internal conviction creates lasting habit.

Two Investors, One Inevitable Outcome

Let's look at the two most common trigger-based investors you will encounter — or perhaps recognise — in India today.

The Gift Card Investor

Priya receives a ₹5,000 mutual fund gift card at her cousin's wedding. She activates it, picks a top-rated fund from an app, and checks it a few times with mild curiosity. Six months later, she has forgotten the password. The investment sits untouched — not growing into a habit, but gathering digital dust.

The FOMO Investor

Rahul hears his office colleague turned ₹2 lakhs into ₹3.5 lakhs in 14 months. He immediately moves ₹1 lakh into a mid-cap fund at its 52-week high. Markets correct 18%. Rahul panics, calls the fund "a scam," exits at a loss — and concludes that investing "doesn't work."

Different entry points. Same exit. The reason lies not in the market — but in the motivation that brought them in.

Think of it like a gym membership gifted on your birthday. You might visit once or twice. You didn't choose it, plan for it, or connect it to a personal goal. Compare that to someone who joins because they have decided to run a half-marathon. Who shows up consistently in February?

The Psychology of FOMO — And Why It Makes You Buy High

FOMO, or Fear of Missing Out, is not a character flaw. It is a deeply hardwired human survival instinct. For most of human history, if the tribe was running toward food, you ran too — or you starved. The problem is that this ancient reflex is perfectly calibrated to destroy modern investment portfolios.

When Rahul sees his colleague's gains, his brain does something specific: it anchors on the peak outcome and ignores the journey. He doesn't ask how long the money was invested, how many sleepless nights were involved, or whether his colleague would have held through a 20% drawdown. He sees the number — and he wants it.

📊What the Numbers Tell Us

- Nearly 4 in 10 retail investors report entering markets after hearing of gains in their social circle

- Over 70% of first-time SIP investors stop within 2 years of starting — most during the first market correction

- The average holding period for first-time equity mutual fund investors in India is under 18 months

- Funds that top annual return charts see 3–5× higher inflows the following year — almost always at elevated valuations

The cruelest part of FOMO investing is that by the time most people hear about the gains, the gains are already gone. You are not buying the opportunity. You are buying the aftermath.

Markets do not ring a bell when they peak. But human psychology does — it is called cocktail-party chatter. When your most financially disengaged friend starts talking about mutual funds at a family gathering, that is often the moment to be cautious, not excited.

The Return-Chasing TrapA fund delivers 45% in a single year. Money floods in at ₹140 NAV. The sector cycle that drove those returns has largely played out. The fund does not know you paid ₹140. And you, with no understanding of why you chose it, have no framework to hold on when it corrects.

The Rollercoaster Every Trigger-Based Investor Rides

There is a predictable, repeatable emotional cycle that almost every FOMO-driven investor goes through. Understanding it is the first step to escaping it.

The Five-Stage Investor Emotion Cycle

The most damaging part of this cycle is not the exit — it is the conclusion the investor draws. "Mutual funds are risky." "Markets are manipulated." "This is not for people like me." These conclusions become permission to never invest again. And they are almost always wrong.

The Gift Card's Hidden Problem

When you decide to invest ₹5,000 yourself, you've gone through something. You calculated the cost. You felt the friction of parting with money. You made a choice. That friction creates ownership. Ownership creates attention. Attention creates understanding. Understanding creates resilience when markets get choppy.

A gift bypasses all of that. The money is "free," so its loss carries little emotional weight — and no motivation to learn, stay, or add more.

Wealth is a Practice, Not an EventThe ₹1,000 SIP you set up and never cancel during a market correction is worth infinitely more than a ₹1 lakh lump sum made during euphoria with no intention to stay invested.

FOMO Investor vs. Process-Driven Investor

| Behaviour | FOMO / Return Chaser | Process-Driven Investor |

|---|---|---|

| Entry trigger | Friend's gains, news, market rally | Personal financial goal defined |

| Fund selection | Top performer of last 1–2 years | Aligned to risk profile & time horizon |

| Investment type | Lump sum at market peak | Monthly SIP with defined tenure |

| When markets fall | Panic, stop SIP, exit | Sees it as buying cheaper units |

| Performance benchmark | Colleague's portfolio, daily news | Progress toward personal goal |

| Typical outcome | Exits early, minimal gain or loss | Compounds wealth over 7–15 years |

How to Invest So You Actually Stay Invested

The good news: these are learnable behaviours, not personality traits. Here is a practical framework to build an investing habit that survives the inevitable ups and downs.

Start With a Goal, Not a Fund

Don't ask "which fund should I buy?" Ask "what am I investing for?" — a child's education, early retirement, a home down payment. The goal gives you a finish line. Without it, every market dip looks like a reason to stop.

Start a SIP — Even ₹500

The amount is almost irrelevant at the start. The habit is everything. A ₹500 SIP that runs for 15 years will teach you more about investing — about patience, compounding, and your own psychology — than a ₹50,000 lump sum you exit after six months.

Understand One Fund Well Before Adding Another

Most new investors diversify too quickly across 8–10 funds they don't understand. Know why you own what you own. If you cannot explain it in one sentence, you don't own it — it owns you.

Never Benchmark Against Your Colleague's Portfolio

Their risk appetite, time horizon, tax situation, and financial goals are not yours. Comparing your returns to theirs is like comparing your exam marks to someone sitting a different paper.

Review Annually, Not Daily

Checking your portfolio every day is like weighing yourself every hour while dieting — the noise drowns the signal. Wealth accumulation happens in years, not minutes. Set a quarterly calendar reminder and close the app.

The Cost of Stopping Your SIP at the Wrong Time

From Chasing Returns to Building Systems

The most important reframe in personal finance is this: stop thinking of investing as a transaction and start thinking of it as a system.

A transaction is "I bought this fund." A system is "I have a SIP of ₹8,000 on the 5th of every month, linked to my daughter's college fund target of ₹40 lakhs by 2038, and I review it every December."

Systems survive market crashes, viral WhatsApp forwards, and the noise of a 24-hour financial news cycle. Transactions do not.

The trigger investor stops here

First market correction. No goal. No conviction. Exit.

The learning investor pauses, then continues

Confused by the dip, but curious enough to understand it. Stays invested.

The process investor barely notices

The SIP auto-debits. More units at lower prices. The goal is 11 years away.

Compounding does its quiet work

The patient investor doesn't talk about it at dinner. The number on the screen does the talking.

Most people who failed at investing didn't fail because markets were unkind. They failed because they were never truly invested — they were speculating on a good feeling that started to fade the moment things got uncomfortable.

Successful investing has never been about finding the right trigger. It has always been about building the right behaviour. Your returns will follow — but only if you stay long enough to collect them.

Ready to Build a System, Not Just a Portfolio?

Talk to a CognityWealth advisor about goal-based investing — a structured approach designed to help you stay invested through every market cycle.

Start the Conversation →